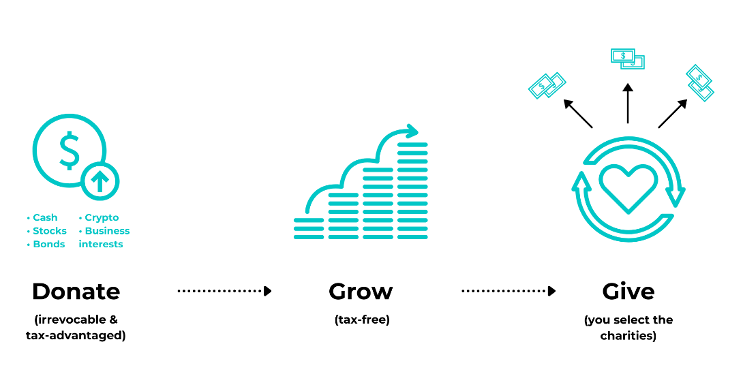

Donor-advised funds have been around for decades, but they’ve only become popular vehicles for charitable giving over the last several years. They offer immediate tax benefits as the assets or funds in the donor-advised fund convey a tax deduction in the year they are gifted. Inside the fund, the assets can grow tax-free and not have to be distributed immediately to a charity.

The funds offer an extremely flexible way to craft a gifting strategy that allows the gift to be invested and managed, to potentially grow over time, and for the gifter to maintain control over the assets.

Understanding Donor Advised Funds

A donor-advised fund (DAF) is a savings vehicle that allows for charitable donations and tax benefits. At the same time, the donor still controls where the assets are to be donated. Donor-advised funds are irrevocable, meaning you can’t withdraw funds after donating. Still, you can specify how the donation is to be invested and to which charity you’d like to donate.

With donor-advised funds, you aren’t limited to donating just cash. Acceptable donations range from stocks and bonds to bitcoin and private company stock.

To ensure a donation qualifies for the full benefits, the fund administrator must be a public charity that falls under the qualifications of a 501(c)(3) organization.

How They’re Managed and How to Contribute to One

First, the donor must open the donor-advised fund at a qualifying sponsor. After selecting a sponsor, donors must make an irrevocable contribution to the fund. At that time, they can take the immediate tax deduction and begin naming beneficiaries and successors for the account.

After contributing, the sponsor firm then has legal control over the funds. It can invest the money per the donor’s recommendations until the donor is ready to decide which charity they’d like to distribute funds to. Since the fund manages the money and handles the administrative tasks that come with donating to charities, administrative fees must be considered when deciding which sponsor to use, as those fees are deducted from the donor’s contributions.

When Does It Make Sense to Contribute to a Donor Advised Fund?

There are many situations where it may make sense to contribute to a donor-advised fund, but some of the most common are:

• If you own highly appreciated assets

• If you’re looking for a tax-deductible transaction

• If you want to make a sizable future donation

The Pros and Cons of Donor Advised Funds

When contributing money to a donor-advised fund, the donor receives an immediate tax deduction on the amount they contributed, even though the funds may not be distributed to a charity until a future date. This allows for greater control and flexibility compared to making a regular donation directly to a charity.

Additionally, contributing to a donor-advised fund makes record-keeping simpler than making multiple donations to different charities and keeping track of all the documents. This is because the fund can act as a “hub” for all gifts. It will record all contributions and provide a single tax document containing all information needed.

Though versatile, many donors are concerned about the fees associated with donor-advised funds. For example, the fund might charge a 1% administrative fee, which is being taken directly from the donated funds. The underlying investments may also have fees, so it’s important that you carefully evaluate where your money is going and how costs play a role in the donation.

The Takeaway

Overall, donor-advised funds are a versatile tool for making donations. They provide tax benefits and allow donors to choose where their money goes. At the same time, those donations can grow tax-free until a charity is chosen. However, there’s more to consider than just the benefits, so to make sure it’s the right move to make for your financial situation, it’s recommended to talk with a financial advisor before establishing a donor advised fund.

This work is powered by Advisor I/O under the Terms of Service and may be a derivative of the original.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.